Recently, The Guardian published a disturbing report about how North Carolina’s Atrium Health—the nation’s third largest non-profit healthcare system—was putting liens on the homes of people unable to pay their medical debts.

There have been thousands of these cases, most involving people who have medical insurance, but whose benefit plans were inadequate to cover massive expenses that follow severe health crises like cancer or major cardiovascular events.

People already burdened with the physical, psychological, and economic strains of a serious illness, or the loss of a loved one, are also facing the possible loss of their homes—the only substantial long-term investment they hold.

North Carolina is a hot spot for these cases, owing to state debt laws that put an automatic lien on real estate assets following any successful debt collection lawsuit. The Guardian notes that the state’s treasurer, Republican Dale Folwell, published a report showing that North Carolina hospitals had filed more than 7,500 lawsuits against indebted patients in just five years. Atrium Health heads the list of collectors.

Atrium is metro Charlotte’s largest hospital system. The company runs 67 hospitals, and over 1,000 clinics throughout the mid-Atlantic and midewestern regions. It employs roughly 150,000 people, has capital assets upwards of $12 billion, and–thanks to its recent merger with Illinois’ Advocate Health–reported $15.2 billion in total revenue in the first half of 2023, and nearly a billion in excess revenue.

Oh, and Atrium Health’s CEO Eugene Woods received a total compensation package of $13.97 million last year, a 40% increase on his already handsome $9.8 million the previous year. According to the Business North Carolina website, 7 other Atrium executives also got compensation packages worth over $2 million in 2022.

People already burdened with the physical, psychological, and economic strains of a serious illness, or the loss of a loved one, are also facing the possible loss of their homes—the only substantial long-term investment they hold.

Though the Tar Heel State leads the nation in medical debt-related real estate liens, and Atrium Health seems to be the most egregious collector, they are certainly not alone. The Guardian’s article cites a Kaiser Family Foundation report showing that the majority of the nation’s 5,100 hospitals are likely using “extraordinary” collection measures, including suing patients, to obtain payments.

CEO Compensation Soars

Keep in mind that Atrium is a not-for-profit system, yet it is putting liens on peoples’ houses while paying its executives seven- and even eight-figure compensation packages.

That should be enough to convince anyone that American healthcare is, basically, a wealth concentration system that functions to enrich the executive class at the expense of patients and practitioners alike.

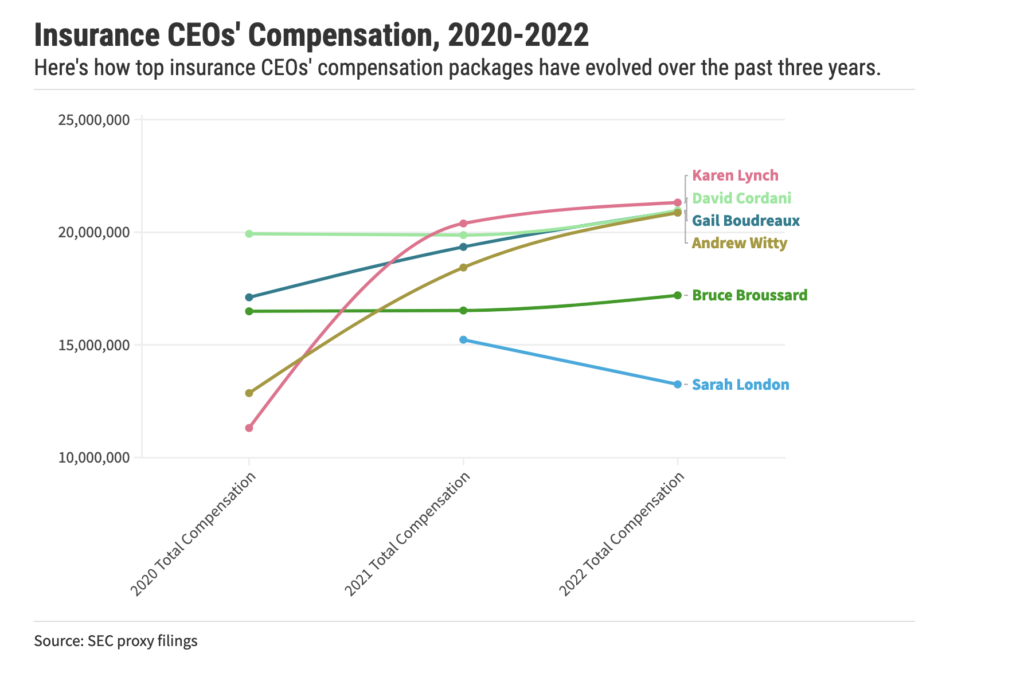

But if you need more evidence, just take a look at the 2022 compensation packages for top executives at the for-profit health insurance companies. Here are the top five highest paid health insurance executives, and their 2022 compensation packages, according to Fierce Healthcare’s annual report on executive compensation:

Karen Lynch, CVS Health (owner of Aetna): $21,317,055 (CEO to median company employee pay ratio: 380:1)

David Cordani, Cigna Group: $20,965,504 (CEO pay ratio: 277:1)

Gail Boudreaux, Elevance Health: $20,931,081 (CEO pay ratio: 383:1)

Andrew Witty, UnitedHealth Group: $20,865,106 (CEO pay ratio: 331:1)

Bruce Broussard, Humana: $17,198,844 (CEO pay ratio: 238:1)

These spectacular executive packages are on top of, and in spite of the fact that administrative waste—defined as unnecessary non-clinical expenses that do not benefit patient care—accounts for roughly 15% of all US healthcare spending.

Wasteful Spending

Up to one-third of all money spent on healthcare goes toward non-medical administrative costs. That’s nearly twice the level seen in other industrialized countries. And the Council on Health Care Spending and Value—a non-partisan consortium of economists and health policy experts—estimates that fully half of this is “wasteful spending,” defined as expenditure that “does not contribute to health outcomes in any discernible way.”

A lot of that is attributable to useless bureaucratic nonsense foisted on medical practitioners and healthcare facilities by the insurance industry.

Bottom line? Executives at health insurance, health IT, hospital management, and pharmaceutical corporations grow increasingly wealthy, while many practitioners struggle to stay afloat, and a huge number of Americans capsize in an ocean of medical debt.

Drowning in Debt

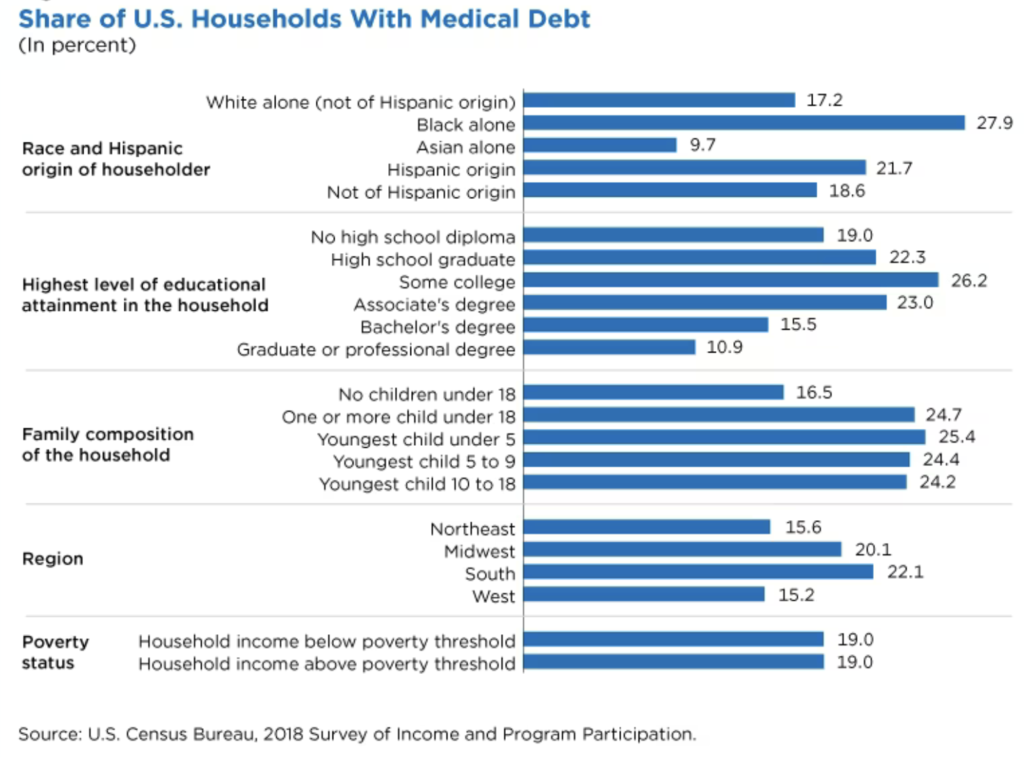

More than half of all US adults (54%) currently have unpaid medical bills, or have had medical debt over the last 5 years, according to the non-profit group RIP Medical Debt. Among people living on less than $60,000 per household per year—which is the oft-cited “400% of the federal poverty level” threshold—67% have medical bills they cannot pay.

Burdensome medical debt disproportionately affects Black people, as well as poor people of all races and ethnicities who are already struggling financially. In many cases, it is quite literally destroying peoples’ lives.

Among people living on less than $60,000 per household per year—the oft-cited “400% of the federal poverty level” threshold—67% have medical bills they cannot pay.

All of these trends have recalled to my mind the interviews I’ve done over the years with Wendell Potter, former director of corporate communications for CIGNA health insurance, and author of, Deadly Spin: An Insurance Company Insider Speaks Out on How Corporate PR is Killing Health Care and Deceiving Americans (Bloomsbury Press).

Revisiting Wendell Potter’s Deadly Spin

First published in 2010, Deadly Spin is a fascinating but disturbing look at the methods by which health insurance companies and their pharma and hospital industry partners collude to shape public perception and manipulate healthcare policy to their own advantage.

Potter, born to poor, hardworking parents in rural North Carolina, and raised in Tennessee’s Blue Ridge Mountains, acknowledges that he became “part of the problem,” as he climbed the corporate ladder in the insurance industry. He writes candidly about the communications playbook by which insurers derailed the Clinton reform plan in the early 90s, de-fanged the Patient Bill of Rights, and remade ObamaCare to guarantee steady profits with minimal regulation, consumer protection, or advantages for clinicians.

“If you were persuaded that the health care reform bill President Barack Obama signed into law was a “government takeover of the healthcare system,” my former colleagues and I earned every penny of our handsome salaries,” he writes.

“The health insurance industry today is dominated by a cartel of large, for-profit corporations. By necessity and by law, the top priority of the officers of these companies is to enhance shareholder value,” Potter says.

Deadly Spin is a primer on corporate propaganda, and it’s a must-read for anyone trying to understand American healthcare, how the system got to be the way it is, and how it perpetuates itself.

Here are highlights, edited for length, from an interview with Mr. Potter that Holistic Primary Care first published nearly 13 years ago. Unfortunately, from the patient and practitioner perspectives, little has changed for the better since 2011. Potter’s comments are as relevant today as they were then.

HPC: Ask physicians what they most dislike about their practices, and “managed care hassles” will be among the top responses. Yet, as you note in your book, organized medicine had a key role in creating and defending the existing system.

WP: Throughout history, the American Medical Association, its membership, and many other physicians’ groups have feared government involvement in health care more they have feared corporate involvement. The AMA has played a lead role in killing any sort of health care reform in this country. The AMA and other physicians’ organizations unwittingly aligned with health insurers to defeat the Clinton plan.

This past time around (the Obama reform plan), they (AMA) ultimately came around to endorse the plan that was finally passed by Congress, which put them at odds with the insurance industry and other special interests. I think doctors are coming to realize that their worst enemies are the corporations that now control the health care system, and that have largely made doctors into indentured servants.

HPC: It seems the insurance industry has done a very good job of deflecting that, because many practitioners view HMOs, managed care and basically any type of health care bureaucracy as “Government Healthcare.” They blame government, and fail to make the distinction between for-profit corporate bureaucracies and the government-funded programs.

WP: They don’t, and that’s certainly something the insurance industry is very happy about. The industry has been engaging in a lot of behind-the-scenes fear-mongering to get people—including doctors—to think that very way.

At the core of all these different efforts to defeat reform is fear-mongering. The insurance industry was very much behind the effort to persuade people that reform…would represent a “government takeover of medicine.” Those were words that were carefully selected to scare people away from reform, and it was very successful.

Among those people scared away were many doctors who just did not stop to give any real thought to what’s really going on. There was not a lot of critical thinking and analysis going on, even among doctors. Many continue to believe that their worst enemy is government, when in reality it is the for-profit sector. Wall Street is dictating how doctors practice medicine far more than they realize.

“The health insurance industry today is dominated by a cartel of large, for-profit corporations. By necessity and by law, the top priority of the officers of these companies is to enhance shareholder value.”

People really don’t grasp that our health care system is largely in the control of for-profit insurance companies. They pretty much set the rules not only for how health care is financed but also for how it is delivered.

Health insurers and pharmaceutical makers are among the most influential lobbyists in Washington, and—in the case of the insurers—the state capitals as well. They’re much more influential these days than the physicians’ groups, even the AMA. In years past, the AMA had been exceedingly influential, but I think it is far less so today, partly because it’s lost a lot of membership, but also because it’s been more or less outgunned by the insurers and other special interests.

Other doctors’ organizations just don’t have the clout. Doctors who embrace holistic care simply don’t have an effective lobby. Doctors’ groups don’t have the financial resources that the big insurers do.

HPC: How would you characterize the relationship between Big Insurance & Big Pharma?

WP: Well, it’s a love-hate relationship. They are often on opposite sides of the bargaining table when the insurers are trying to cut deals to save money on medications. But they are mutually dependent on each other. There’s a symbiotic relationship. They need each other, and they often are aligned on the same side of policy. They were aligned very closely to defeat the Clinton plan, and they’ve been on the same side to try to defeat other health reform measures. They share common interests. One in particular is a dislike of any kind of government regulation. It’s the one thing they truly share in common, and they can usually find enough common ground on that to help defeat any reform legislation, even if their business objectives are often very different.

HPC: Have you seen them working together directly?

WP: Oh, yeah! I was a representative for one of the insurers I worked for to an organization in Washington called the Healthcare Leadership Council. And the pharmaceutical companies have membership in that group, as do many of the large insurers. And that group played a big role in killing the reform plan as proposed by the Clintons, and also in the effort to kill the Patient’s Bill of Rights proposals back in the late 90s and early 2000s.

HPC: The insurance industry has shown a remarkable ability to stand united when confronted with policy challenges. How are the companies able to overcome their competitive imperatives and work so closely together?

WP: They know it is important for them to speak with one voice and that that voice be consistent. They are disciplined. America’s Health Insurance Plans (AHIP), their national trade association, is the enforcer of that discipline and the place where all the messaging originates. There is no single association that speaks for physicians the same way that AHIP and the Blue Cross Blue Shield Association speak for insurers.

“If your employer doesn’t cover you, and you can’t afford to buy it, and you’re not eligible for Medicare or Medicaid, you’re pretty much out of luck. If you don’t have coverage and you don’t have a significant income, you’re going to forego care. That is de facto rationing! It’s happening every single day in this country.”

HPC: Many Americans believe the US has, “the greatest health care in the world,” despite much evidence to the contrary. They also believe reform will diminish this greatness and stifle innovation. Is this an example of industry spin?

WP: I don’t know the exact origins of that idea, although it is oft-cited by opponents of reform. We do have some of the best doctors and other caregivers, and some of the best facilities and technologies. But we also have one of the most inequitable systems in the world, behind Bangladesh in fairness, as I note in the book. As far as medical innovation, the truth is that much of the innovation comes from government entities such as NIH and other places. For-profit companies profit from their work.

“There is no single association that speaks for physicians the same way that AHIP and the Blue Cross Blue Shield Association speak for insurers.”

HPC: Your book sheds much light on the ways insurers use and manipulate ideas and words. What’s the history of the word “provider?” Years ago, doctors actively resisted that term. Now, it seems most are resigned to it.

WP: Well, it is. The insurance industry decided to go with a term like that to be able to refer to all health care practitioners and facilities with one word, because it embraces hospitals and a full spectrum of clinicians. Another reason is that insurers know that doctors are held in higher esteem than insurance companies, and they are loathe to use the word “doctor” or “physician” if they can avoid doing it.

HPC: Years ago, we used to hear the term, “rationing” quite often, though this word has fallen out of favor. Yet, isn’t that exactly what our system is based on? Aren’t health insurance companies rationing care?

WP: Oh, absolutely. People are not fully aware of how it works, but the insurance industry rations care in a much less equitable way than any other system that I know of. The industry’s business practices in and of themselves result in rationing. We have 52 million people in the US who don’t have coverage, largely because of the practices of insurance industry. The benefit plans are just not affordable for so many Americans.

If your employer doesn’t cover you, and you can’t afford to buy it, and you’re not eligible for Medicare or Medicaid, you’re pretty much out of luck. If you don’t have coverage and you don’t have a significant income, you’re going to forego care. That is de facto rationing! It’s happening every single day in this country.

The other thing is that even for those who do have insurance, there are executives and managers that make rationing decisions every day, when they make decisions to deny coverage for one thing or another. Even the ‘not for profits’ like the Blue Cross/Blue Shield plans play this way. So, rationing is done in this country. But in many cases, it is done by a manager at a for-profit corporation, who knows he or she has a job to do, which is to make sure the company meets Wall Street’s profit expectations.

HPC: Despite widespread public interest, and growing scientific support, insurance plans have been very slow to embrace holistic medicine, nutrition, supplements & other aspects of preventive medicine, even though it could save money down the road. Why?

WP: For one thing, the insurers don’t know or haven’t seen sufficient evidence that holistic medicine could help them lower cost. If they can be made to understand that a holistic approach could actually lower their cost, then I think they would embrace it. But they haven’t been persuaded of that so far. They’re very focused on short-term profitability, and they know there’s a great deal of turnover in plan membership. So they don’t want to spend a lot of money providing preventive care to people right now who in one, or five, or 10 years will no longer be enrolled in their plans. The plans won’t do anything unless they believe it will have benefit on profitability.

END