Nearly 60% of holistic medical practitioners now routinely offer remote consultations, according to a new survey of more than 1,100 clinicians. Nearly 90% of those who use telemedicine platforms are satisfied with the experience. (Image: TippaPat/Shutterstock)

Telemedicine

is now commonplace in holistic medical practices, and practitioners who offer

teleconsultations are very satisfied with the experience.

That’s

one of the main findings from Holistic Primary Care’s 2023 practitioner

survey, conducted over the summer in collaboration with Nutrition Business Journal.

The 70-question survey covered a

broad range of topics—from the impact of the Covid pandemic to the role of

dietary supplements and herbs in patient care. We gathered data from 1,151

practitioners representing diverse clinical disciplines and modes of practice.

The participants were drawn from Holistic

Primary Care’s readership, and from the client databases of several

prominent practitioner-focused supplement companies via Nutrition Business

Journal.

Age-wise the cohort skewed older:

54% were between the ages of 45 and 64 years old, and 24% were 65 and above,

while 17% were under 45. Three-quarters of the cohort have been in practice for

at least 10 years, and 29% have been practicing for 30 years or more. The majority

of respondents were female (61% versus 32% male), a trend we’ve observed in

most of our past surveys.

The cohort included responses from

(in descending order): chiropractors, medical doctors, naturopathic doctors,

nurses, wellness coaches, acupuncturists, dietitians and nutrition

professionals, as well as a smattering of other practitioner types.

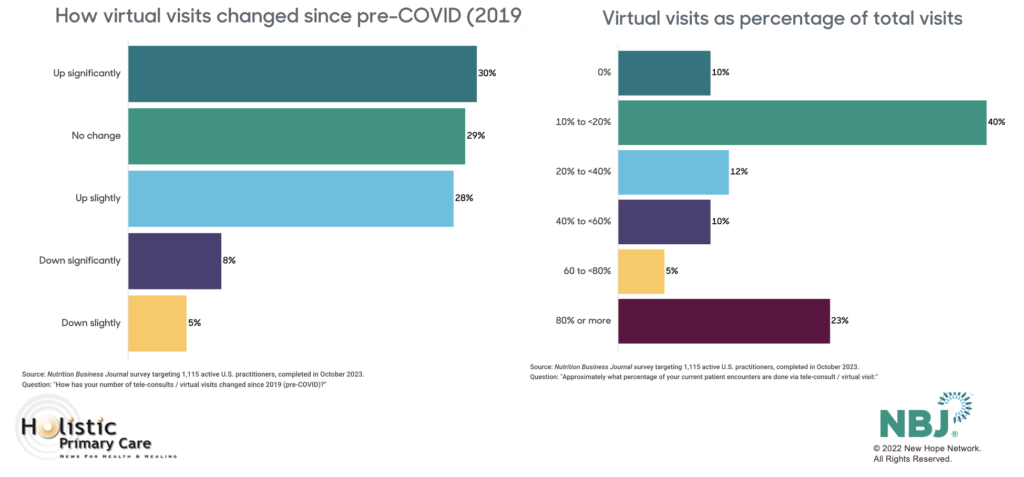

Virtual Visits Surge

Telemedicine, which grew exponentially

nationwide during the Covid pandemic, was an important theme in this year’s

survey, as we sought to understand the impact of this technological phenomenon

on holistic practices, and on the relationships between practitioners and their

patients.

Fifty-eight percent of our survey

respondents indicated that they currently provide virtual visits for at least

some of their patients, and 30% report that their volume of virtual visits

increased significantly since the Covid pandemic. Another 28% said teleconsults

are up slightly since the start of the pandemic.

We expected to see a large

age-associated variation in engagement with telemedicine. The data did indicate

a somewhat greater level of engagement among younger practitioners: 66% of

those under the age of 45 offer virtual visits, versus 55% among the clinicians

over age 60. But that difference was not dramatic, and telemed engagement is

high in all age brackets.

It was also high across all

practitioner types and practice settings, though the number of respondents

offering virtual visits was quite a bit higher among practitioners with

conventional allopathic training (the MDs, DOs, RNs, NPs) compared with the

DCs, NDs, and others with non-allopathic “alternative medicine” training (73%

vs 54%).

Most practitioners say their volume of virtual visits has increased since the Covid pandemic. For nearly one-quarter of respondents, teleconsults represent 80% or more of all patient encounters.

There’s no question that

teleconsults have become a routine part of patient care in many clinics, but

they haven’t entirely replaced old fashioned face-to-face visits. The majority

of practitioners (62%) currently offering virtual visits say these represent

less than 40% of total patient encounters. Fully half say virtual visits make

up less than 20% of all visits.

That said, for almost one-quarter

of these practices (23%), virtual visits account for 80% of all encounters.

Satisfaction is High

Practitioners

who use telemedicine like it a lot: 45% describe themselves as “very satisfied”

with their telemedicine experience, and 41% say they’re somewhat satisfied. In

contrast, only 14% expressed any degree of dissatisfaction.

Our

findings track with general trends seen throughout healthcare. According to a large

nationwide survey of office-based physicians published early in 2023 by the Office of the

National Coordinator for Health Information Technology (ONC), the number of

doctors using telemedicine increased six-fold from 15% in 2018, to 87% by the

beginning of 2019.

The

spectacular growth of virtual visits over the last five years was driven

largely by necessity during the first year of the pandemic, when the virus was

spreading rapidly, many people were dying or severely ill, and in-person

medical encounters suddenly became a high-risk proposition.

It

was also fueled by a “temporary” suspension of HIPAA (Health Insurance

Portability & Accountability Act) regulations that had, prior to Covid,

hindered the evolution of telemedicine. Massive federal and regional government

spending on telehealth infrastructure and oversight, combined with enthusiastic

investment from Big Tech and venture capital also played a role.

Our stats

on telemedicine use are not quite as high as ONC’s, but this is not surprising

because the ONC survey showed that the largest growth in telemedicine was among

practitioners in large group practices, and in Patient-Centered Medical Homes

or Merit-Based Incentive Systems practice models. These are not practice

settings that have typically been friendly to holistic and functional medicine.

The

HPC/NBJ cohort is largely comprised of practitioners in solo (70%) or

small-group practices (19%), and direct cash-pay (54%) or mixed cash/insurance

(28%) practice models.

Limitations of Virtual Visits

Further, there are many holistic modalities—chiropractic adjustments, acupuncture, and massage, for example—that simply cannot be done remotely. And much of the appeal of holistic medicine, for patients and practitioners alike, is its relationality and direct emotional connection. To some extent, these aspects are diminished in a techn-mediated remote encounter.

In terms of improving access, telemedicine has been a big plus for many people, especially those in rural areas who live far from the nearest clinic, and also those whose mobility is limited by age, illness, or disability. It provides unparalleled convenience, particularly when they need attention for minor health concerns or follow-ups, that don’t really require in-person contact.

According

to a Kaiser

Permanente survey of 1,000 northern California patients who’d had

remote consults with Kaiser physicians between March and October 2020, 80%

reported that the virtual visit(s) met their medical needs as well as in-person

visits, and almost 20% said they actually preferred seeing their doctors

remotely rather than in person.

Metova,

a custom software provider, fielded a

survey of over 1,000 people in the summer of 2020, and found that 80% of those who’d

experienced a virtual visit would gladly choose telemedicine for subsequent

visits if given that option.

All

that being said, telemedicine does have its drawbacks. Though it can improve

patient access to care in some cases, it also categorically excludes people who

do not have mobile phones or computers.

Who’s Excluded?

Jacqueline Fincher, MD, a rural primary care physician in Thompson,

GA, and president of the American College of Physicians from 2020-2021 at the

height of the pandemic, told Holistic Primary Care that in her area of

eastern Georgia, many of the people who would potentially benefit from

telemedicine have no way to access it.

“It takes good audio and video on both ends—the patient and the

practitioner—for remote consults to work. At least 30% of the time, at least

one of those parts doesn’t work properly. Sometimes, it’s just not an option in

rural areas, because the (internet) bandwidth just isn’t there to support it.”

Dr. Fincher added that in her area, a majority of her most

vulnerable patients—the poor, the elderly, the less educated—do not own

smartphones, laptops, or any other digital technology. “I still have a lot of

patients who are using landlines only. I can talk with them, but I can’t see

them, can’t observe them. It is very limited.”

A 2021 report by

the Pew Research Center shows that while mobile phone ownership is very high in the US,

approximately 15% of the adult population does not own a smartphone.

Great…When It Works

And like all things technological, virtual visit platforms are

wonderful when they work properly….but often enough, they do not. Tech glitches

can cause consternation for practitioners and patients alike.

In 2022, UnitedHealth Group and Optum posted a survey of 240 practitioners representing a wide range of specialties and practice settings. While 69% described telemedicine as “convenient,” 28% said their first-choice descriptor was “frustrating.” Half said they experienced difficulties navigating the teleconsult platforms.

Surveys of patients show a similar aggravation with the technology. Further, some patients report that they have difficulty finding quiet private places at home or in their offices, in which to have consultations with medical professionals. And on both the practitioner and patient side, there are concerns about confidentiality, and the possibility that hackers could access the platforms and steal intimate personal information.

Telemedicine

will never entirely eliminate in person clinic visits. But our survey and many

others show that for many medical practices—including holistic, functional, and

even chiropractic clinics—it has become a prominent part of day-to-day patient

care. And for nearly a quarter of our respondents, virtual visits are the main

mode of contact with patients.

Though it has some drawbacks, the benefits of telemedicine far outweigh the downsides, and it will be an increasingly important facet of healthcare in the years to come.

Nutrition Business Journal’s comprehensive 2023 Healthcare Practitioner Channel report, based on the complete data set from our collaborative survey, is available for purchase at: https://store.newhope.com/pages/nbj-2023-reports.

Lab work.

It is an essential part of any medical practice, especially in functional

medicine clinics. It can also be a big hassle factor for practitioners and

patients alike.

While

companies like Quest and Labcorp have done a good job of bundling standard

conventional lab tests into single one-stop shops, so to speak, the situation

within functional medicine is more complex.

Practitioners

routinely deal with multiple lab companies, each with its own offerings, its

own timelines, and its own idiosyncratic methods. There’s the challenge of

ordering and stocking test kits to give to patients. And that’s on top of the

general headaches of scheduling blood draws when needed, chasing and

aggregating test results, and booking patient visits to discuss them.

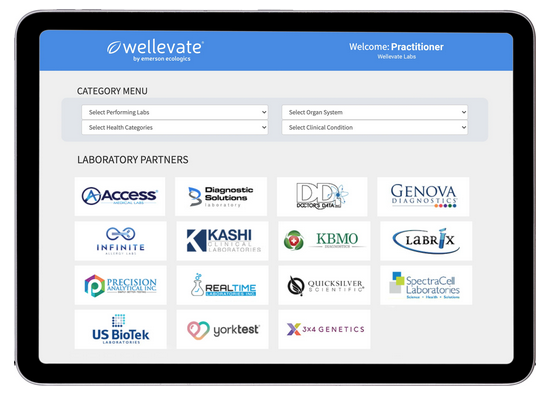

With its new Wellevate Labs platform, Emerson Ecologics—one of the nation’s major practitioner-focused supplement distributors—aims to take the hassles out of functional diagnostic testing with a one-stop digital platform through which practitioners can order tests, store results, schedule visits, and develop care plans.

Simplicity

& Continuity

Emerson’s

fully HIPAA-compliant Wellevate “Connected Care Platform” launched in

November 2020. The lab management component is the latest inclusion in an

already robust set of practice management tools that includes a secure

telemedicine system (powered by Vsee). Qualified

practitioners can access the Wellevate suite free of charge.

“Diagnostic

and functional testing labs are so disparate. Practitioners have to maintain

all these relationships with different labs, deal with multiple portals, keep

supplies of test kits. Our goal is to simplify all of that,” explains Jaclyn Chasse

Smeaton, ND, Senior Vice President of Medical Affairs at Emerson

Ecologics.

Jaclyn Smeaton, ND

The

lab management project was driven, in part by the new healthcare dynamics

brought about by the COVID pandemic.

Emerson

saw a major surge in Wellevate users since the pandemic began, as practitioners

and their patients sought online substitutes for in-person clinic visits. On

the supplement dispensing side, the company saw a big rise in product sales in

early 2020 that has stayed consistent throughout 2021.

But

the Wellevate team was aware that the pandemic has been extremely challenging

for many clinics.

Born

From Pandemic Pressures

“When

the pandemic hit, we were very worried about the small, solo practitioners,” says

Smeaton, who still maintains a small private naturopathic practice of her own.

Independent

practices make up a significant proportion of Wellevate’s practitioner base.

While many small practices were struggling to stay afloat, Smeaton and her

colleagues saw that others were thriving despite the pandemic.

“Some

were even doing better than before. So, we phoned them to ask about what they

were doing and how they were making it work, so we could share those tips with

others.”

Among

the gleanings, Wellevate learned that many practitioners wanted ways to

simplify lab work. Input from the clinical community shaped Wellevate Labs, as

well as other innovations like Wellevate’s “Pivot Your

Practice”

practitioner education campaign.

The

lab venture draws on Emerson Ecologics’ 40 years of experience and expertise in

aggregation and distribution.

“We

had already developed solutions to help practitioners dispense a wide range of

different supplements from diverse companies,” Smeaton explained. Aggregation

of lab tests, simplifying the ordering process, and consolidating the results

was a similar multi-vendor distribution challenge.

The

venture also benefits from a creative partnership with Evexia

Diagnostics, a practitioner-founded practice management company that has been a

pioneer in lab test aggregation. Evexia provides the software infrastructure

for Wellevate Labs.

A One-Stop

Portal

As

with its online dispensary, Wellevate Labs is a one-stop portal through which

practitioners and their patients can access the vast majority of common lab

tests—standard conventional panels as well as “specialty” functional medicine ones.

Wellevate

maintains the relationships with the various lab companies, obviating the need

for practitioners to do so. On the front end, like their virtual dispensary,

the lab platform is fully customizable with a practice’s graphics, color

schemes, and patient-facing editorial content.

Wellevate

currently offers tests from 16 major specialty labs including Genova

Diagnostics, SpectraCell, Doctor’s Data, Precision Analytical, US BioTek, and

Diagnostic Solutions. Clinicians can also use Wellevate to order conventional

tests via Labcorp, though these appear as a separate order on the portal’s

dashboard.

Wellevate

Labs already has roughly 650 users, with more logging on every week. Smeaton

says onboarding and implementation is quick, especially for practitioners

already using the basic Wellevate platform. Most clinics can get the system up

and running in a matter of minutes.

Wellevate

Labs does require users to enter NPI (National Provider Identifier) numbers, to

validate medical credentials. The platform is accessible to all physicians with

prescribing rights. In states where they are licensable, naturopaths can access

it independently. NDs in unlicensed states, chiropractors, nutrition

professionals and others can use Wellevate Labs but only under MD

oversight.

Seamless

Orders

On

the practitioner side, ordering tests for a patient is as simple as clicking the

name of the lab(s), and then clicking the desired tests. The system offers some

pre-set combination panels that aggregate diverse tests from different labs. It

also allows practitioners to customize their own test combos.

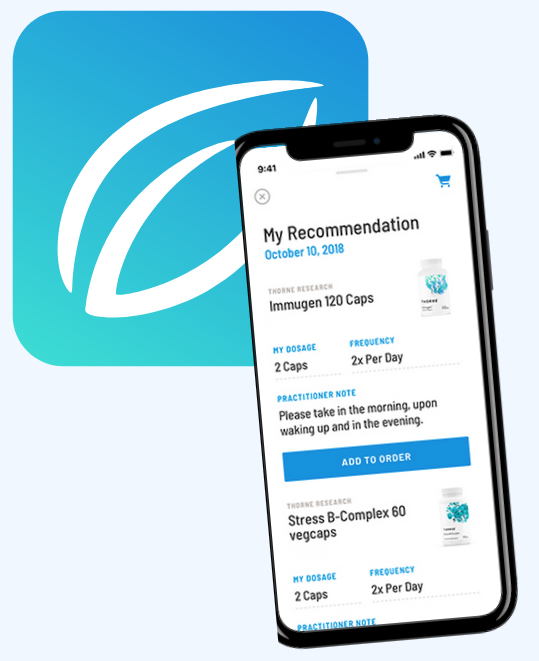

On

the patient side, the Wellevate app shows patients what tests their doctors have

requested with complete price transparency, since most specialty tests are not

insurance reimbursable. Once the patient

affirms the order and pays, the test requests are automatically sent to the

labs.

If a

particular test requires a kit or special supplies, the labs send them to the

patient, or to the clinic if need be.

“It’s

really seamless. There’s one order, and one checkout, with no balance billing.”

Patients

and practitioners can also use the app to schedule phlebotomy appointments at the

clinic, in the patient’s home, or at any Labcorp draw center. They can also use

the app to review care plans and supplement recommendations, and to order

refills.

Once

tests are completed, the labs report the results directly into the Wellevate

platform where they become visible to practitioners and patients for review.

This facilitates interpretation, discussion, and care planning.

Wellevate

handles all patient tech support calls, freeing practitioners from the need to

talk patients through logistics, answer common questions, or troubleshoot

glitches.

Competitive

Pricing

Functional

diagnostic testing can get expensive; the Wellevate team is conscious of this

fact. Smeaton says the platform offers specialty tests at the lowest allowable

prices, and that Labcorp has given them very good rates on conventional tests.

The

proximity of this new test aggregator and Emerson’s supplement dispensary

inevitably begs the question of conflict of interest: Will practitioners order

tests with the unstated goal of driving supplement sales revenue?

Smeaton

says it is a reasonable question for someone to ask. But she stressed that the

potential for conflicts of interest exists whenever a patient is purchasing

anything from a medical practice. “Wellevate does not change that in any way.

It still comes down to whether a patient can trust that a practitioner has

their best interests in mind.”

She

stressed that the new labs platform is fully HIPAA-compliant, and that

Wellevate takes cybersecurity very seriously. The platform does not store any

patient credit card information, and Emerson’s information security team works

with independent third-party consultants that monitor the system for

vulnerabilities.

Smeaton

and her colleagues expect that the Wellevate Labs platform will continue to

expand and improve as more practitioners use it, and more lab companies offer

their tests.

Telemedicine has been the big winner in the COVID economy, and

growth of this sector has shown no sign of slowing.

In 2020, as the COVID-19 crisis forced practitioners, patients, and

legislators to recognize the need for expansion of telehealth, the global

market for digital healthcare services reached

an estimated $152.5 billion. Researchers project that the industry —

which comprises digital health systems, healthcare analytics, and telemedicine

— will grow to $456.9 billion by 2026.

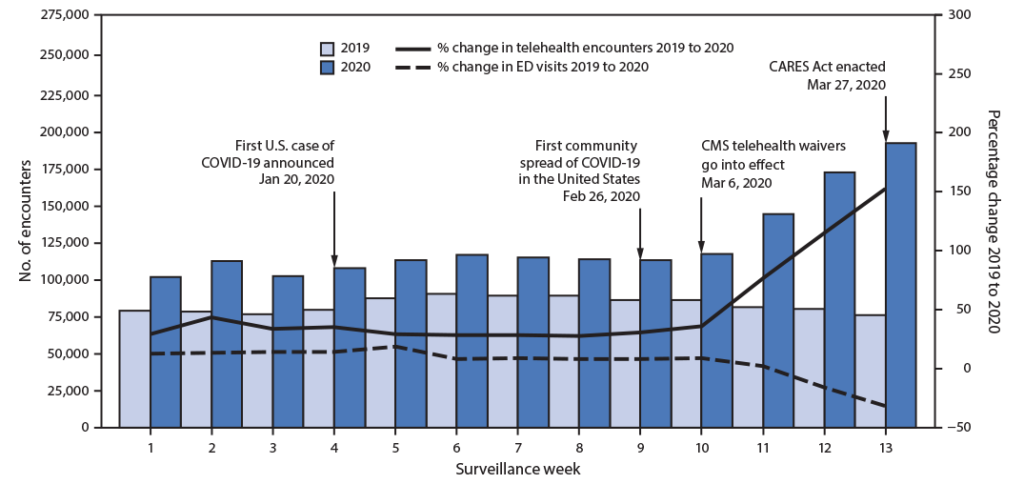

Number of telehealth patient encounters reported by four telehealth providers that offer services in all states and percentage change in telehealth encounters and emergency department (ED) visits — United States, January 1–March 30, 2019 (comparison period) and January 1–March 28, 2020 (early pandemic period) Source: Centers for Disease Control & Prevention

The use of telemedicine services in particular skyrocketed in early

2020. A CDC report shows that in the first quarter of that

year, the number of virtual healthcare visits increased by 50%, compared with

the same period in 2019. In the last week of March 2020 alone, telemedicine

visits jumped 154% over the number of visits that same week in 2019.

That acceleration continued in 2021. By one account, ten times more telehealth visits

occurred in March 2021 than in March 2020.

Big Tech is paying attention to these trends. About a year ago,

Google announced a major $100 million investment in

Amwell, one of the largest telehealth service providers.

Amwell’s revenue jumped from $69 million to $122 million — a 77%

increase — in the first six months of 2020, according to its IPO filing. Alongside other recent developments the

company noted the significant reduction of regulatory and reimbursement

barriers for telehealth, surging demand for on-demand remote COVID-19 services,

and a desire to protect healthcare workers and patients from people infected with

coronavirus.

Stay-at-home orders and business closures also boosted the

popularity of fitness apps and “smart” exercise equipment.

Millions of smartphone users downloadedmeditation and sleep apps like

Calm and Headspace, programs that promise better rest, lower stress, and less

anxiety.

A host of digital health platforms now offer quick, discreet,

on-demand access to medical services. They can also eliminate long wait or

travel times to receive medical attention. The trade-off for convenience means

that health tech users accept the risk of their sensitive personal data being

hacked or used in ways that aren’t initially intended or clearly disclosed.

Threats to data privacy have worsened since the pandemic began.

Cyberattacks on healthcare institutions spiked last year, as Forbes and others reported earlier this Summer. For the fifth

straight year in a row, hacking incidents rose again in 2020, up a striking 42%

from 2019.

The increase in healthcare hacking events raised enough red flags

that in October 2020, the Cybersecurity and Infrastructure Security Agency,

Department of Health and Human Services, and FBI issued a joint cybersecurity advisory warning

of “an increased and imminent cybercrime threat to U.S. hospitals and

healthcare providers.” They cautioned healthcare institutions to “ensure

that they take timely and reasonable precautions to protect their networks from

these threats.”

Leaked healthcare data — the presence of pre-existing conditions or

potentially “embarrassing” diagnoses — can unknowingly affect the ability to

obtain life insurance, the amount paid for coverage, or the interest rates

they’re charged on loans. In the wrong hands, health data shared without a

patient’s knowledge can also result in workplace discrimination.

Over the last five years, nearly all of the major information

technology companies have launched some sort of healthcare initiative. The

COVID pandemic, with its surging demand for telemedicine and rapid exchange of medical

data, only intensifed that trend.

But some tech giants have learned the hard way that healthcare is

very different from other business sectors.

Successful or not, Big Tech’s healthcare ventures raise profound

ethical questions about the uses of personal medical data and the limits of

privacy in the digital age.

Haven & Hell

Haven was founded on the lofty goals of improving healthcare

services and lowering medical costs for employees of the three founding

companies, an aggregate workforce of roughly one million people.

The venture started out strong in 2018, but proved to be short-lived.

By early 2021, barely three years after its launch, Haven posted a vaguestatement on its now defunct website announcing

plans to disband.

Many healthcare analysts have opined on why Haven hit the rocks. CNBC

reported that

despite the outward appearance of collaboration, “each of the three founding

companies executed their own projects separately with their own employees,

obviating the need for the joint venture to begin with.”

Other speculations cite sluggish progress, high executive turnover,

lack of “bold ideas,” absence of “strategic clarity,” and the company’s status

as a not-for-profit rather than a profit-driven venture.

But it might also be

that Haven’s leaders simply overestimated their own strengths and

underestimated the depth of healthcare’s quicksand. The hiring of a few medical

superstars like surgeon/author Atul Gawande, MD, and former ZocDoc chief technology

officer, Serkan Kutan, was not enough to transform an online retailer, an

investment bank, and a corporate holding company into a healthcare business.

“A real

possibility is that the entrenched complexity of the American healthcare

business model proved too daunting to change. As large as these parent

organizations are, they still don’t possess the economies of scale to tip the

balance when it comes to healthcare,” said Lyndean Brick, president

of healthcare consulting firm Advis, in an article

published by Fierce Healthcare.

Many healthcare analysts have opined on why Haven hit the rocks. Speculations cite sluggish progress, high executive turnover, lack of “bold ideas,” absence of “strategic clarity,” and the company’s status as a not-for-profit. But it might also be that Haven’s leaders simply overestimated their own strengths and underestimated the depth of healthcare’s quicksand.

Moving forward,

Amazon, Berkshire Hathaway, and JPMorgan Chase have stated—in perfect

corporate-speak–that they will “leverage the insights” gained from Haven, and

will “collaborate informally to design programs tailored to address the

specific needs of their own employee populations.”

Healthcare

on Demand

Amazon seems undaunted by the Haven debacle; the company has forged

on with several independent healthcare ventures.

Earlier this year, it confirmed plans to broadenAmazon Care–a virtual healthcare service previously

available only to Amazon employees—to other big employers.

Amazon Care was piloted in 2019 as a benefit for Amazon workers and

their families in the company’s home state of Washington. This Summer, it

extended the virtual service to all its US employees.

Successful or not, Big Tech’s healthcare ventures raise profound ethical questions about the uses of personal medical data and the limits of privacy in the digital age.

Aspects of Amazon Care resemble other well-established telehealth

services. To begin using the app, patients answer questions about their

physical and mental health. Users can then schedule medical visits and chat

with nurses or doctors via video or messaging features. Amazon claims employees

are typically able to connect with medical professionals in less than 60

seconds.

Image: Mundissima/Shutterstock

Along with virtual care, the system also provides options for

in-person services. Patients can request home or office visits for COVID-19 and

flu testing, vaccinations, illness and injury treatment, preventive care,

routine blood draws, sexual health services, prescription requests, refills,

deliveries, and more.

Amazon ambitiously aims to bring its virtual and in-home healthcare

platforms to at least 20 major

US cities in 2021 and 2022. The company also plans to expand Amazon

Care beyond its own employee base by “supplying” it as a workplace benefit to

other companies.

The paradox is that as Amazon strives to be a healthcare leader, it

simultaneously faces accusations of unsafe working conditions and employee

abuse.

During the “heat

dome” weather event last summer, indoor temperatures at an

Amazon warehouse in Washington state allegedly reached 90 degrees. Despite the

extreme heat and lack of adequate climate control, workers were asked to move

as quickly as possible to “boost productivity,” theSeattle Times reported. This follows many prior

charges from Amazon employees who’ve described unhealthy working conditions

while being treated “like robots.”

Beyond

Amazon Care

Amazon Care is not the tech titan’s only foray into healthcare. Its

most recent is a direct-to-consumer at-home COVID-19 test kit.

Last Spring, the Food and Drug Administration issued anEmergency Use Authorization for

Amazon’s real-time RT-PCR test for SARS-CoV-2. Customers can now order these Amazon

COVID-19 test kits through the company’s diagnostics site,AmazonDx.com, by

providing the same login credentials used to access its online shopping site.

Amazon hinted at further moves into diagnostics, including tests for

respiratory infections and sexually transmitted diseases, Business Insider

recentlyreported.

Last June, Amazon Web Services (AWS) unveiled theAWS Healthcare Accelerator, a four-week “technical, business, and mentorship accelerator

opportunity” for fledgling digital health companies.

The paradox is that as Amazon strives to be a healthcare leader, it simultaneously faces accusations of unsafe working conditions and employee abuse.

According to a blog

post from Sandy Carter, AWS’ vice president of worldwide public

sector partners and programs, the Accelerator is specifically focused on

startups seeking to “accelerate growth in the cloud.” The program is now

accepting applications from up-and-comers looking to leverage Amazon’s

technical and commercial expertise “to help solve the biggest challenges in the

healthcare industry.”

The Accelerator will focus on “solutions” — a favorite tech

industry term — such as remote patient monitoring, data analytics, patient

engagement, voice recognition, and virtual care. By using AWS, Amazon says

“organizations can increase the pace of innovation, unlock the potential of

data, and personalize the healthcare journey.”

Data

Fuels Deep Learning

But what exactly is the “potential” of data? And who does it really

benefit?

Among the more revolutionary developments in IT are data-driven

“smart” machines, which use artificial intelligence to “think” and act like

humans.

One branch of AI, called deep learning, relies on algorithms that

mimic the neural networks of the human brain. Like the brain, AI-based machines

continually receive and process large amounts of data, and teach themselves new

tasks based on what they glean.

People across the globe generate huge amounts of data every day,

all of which — when captured — fuels the deep learning process. The more

information the algorithms take in, the better they become at predicting

outcomes — including things like human behaviors, disease progression, and

treatment responses.

Image: Ryzhi/Shutterstock

Most of our digital gadgets now rely on machine learning to some

extent. Virtual assistants like Amazon’s Alexa or Apple’s Siri use AI to

decipher users’ unique speech and language patterns. Driverless AI-guided vehicles

learn not only the mechanics of driving, but how to respond spontaneously to

unexpected obstacles or occurrences.

Whether or not users realize it, social media platforms like

Facebook, Twitter, and Instagram continuously collect and analyze personal

behavioral data. Our data is, essentially, a form of payment to access these

“free” online services. AI-based programs glean information about our favored

activities, habits, aesthetic preferences, socioeconomic status, political

inclinations, and our health.

Presently, the US does not have comprehensive consumer data privacy regulations governing what can and cannot be done with data that users enter into online apps. Instead, we have a patchwork of inconsistent state-level regulations.

Amazon, with its diverse healthcare operations, are no doubt

amassing astonishing amounts of medical information. So are most of the

high-tech healthcare companies.

Big Promises, Big Problems

Proponents of AI present it as a powerful problem-solver that helps

us overcome the limits of our own brains. Because machines can process much

larger quantities of information than can the human brain, AI expands our

ability to think creatively and develop novel solutions to serious problems.

Tech companies say they use AI to enhance the “user experience.” In

healthcare, the rationale is usually “to improve clinical outcomes,” to “reduce

complexity,” to “streamline the patient experience” or some similar pastel-toned

platitude.

And there’s no question that AI does hold great promise for

improved patient care. One of the most exciting medical applications is in the

detection of cancer.

An article published last year in Nature describes an AI

technology “capable of surpassing human experts in breast cancer prediction” (McKinney, S et al. Nature. 2020; 577: 89–94). The AI system’s ability to interpret

mammograms outperformed humans in detecting both false-positive and

false-negative results.

Researchers have also used artificial neural networks to predict

the likelihood of recurrence within 10 years following breast cancer surgery.

One group posits that accurate predictions by machine learning algorithms “may

improve precision in managing patients” post-surgery and increase the

understanding of risk factors for breast cancer recurrence (Lou, S et al. Cancers (Basel). 2020; 12(12): 3817).

But the price for AI-enhanced healthcare is loss of privacy.

Flow of

Information

Take, for instance, AI-driven menstrual trackers. The popular

menstrual app,Flo, which is used by an estimated 100

million women, offers what claims to be “the most precise AI-based period and

ovulation predictions by tracking 70+ body signals like cramps, discharge,

headaches and more.”

Flo users enter a host of health details related to their menstrual

cycles and sexual activity, and the app tracks period symptoms and fertility

patterns. The company says it helps users determine whether their cycles are

“normal” or “irregular.”

Similarly, Apple iPhones contain a built-in app whose features

include menstrual cycle tracking. Applesays the tracker will “improve predictions

for your period and fertility window.”

While menstrual tracking apps might offer benefits like helping couples

to either achieve or avoid pregnancy, they also raise significant safety and

privacy concerns. In exchange for period-tracking services, patients provide the

tech companies — and potentially others — with a wealth of very personal

information.

The price for AI-enhanced healthcare is loss of privacy

Researchers have questioned both the reliability of fertility apps and

the unregulated nature of the market (Ali, R et al. Repro BioMed Online. 2021; 42(1) 273-281). One

study from 2020 looked at 140 different menstrual apps and concluded that while

some are accurate and useful, “many more are of low quality, and users should

be wary of relying on their predictions to avoid pregnancy or to maximize

chances of conception.”

Some menstrual trackers, including Flo, have significant data

privacy flaws and they have been called out for sharing user data despite

promises to keep that information private. In 2019, a Wall Street Journal investigation

revealed that the app shared users’ intimate reproductive and sexual health data

with Facebook, Google, and other third parties that provided marketing and

analytics services for Flo.

According to Consumer Reports,

analysis of privacy and data security practices of Flo and four other period

trackers showed that users receive no guarantee that their data would not

be shared with third parties for marketing or other purposes.

Following a 2020 complaint, the Federal Trade Commission announced last January that it had reached a

settlement with Flo. Among other requirements, it mandates

that the company must obtain users’ consent before sharing their health

information.

Lack of

Oversight

Presently, the US does not have comprehensive consumer data privacy

regulations governing what can and cannot be done with data that users enter into

online apps. Instead, we have a patchwork of inconsistent state-level regulations.

There are data privacy laws governing specific sectors, including

healthcare. The best known is the Health Insurance Portability and

Accountability Act of 1996 (HIPAA). Other laws also regulate electronic health

records systems and telehealth technologies.

But in the post-COVID world, many of HIPAA’s protections have been

curtailed.

Early in the pandemic, the Department of Health and Human Services (HHS) — the entity charged with enforcing HIPAA — announced a temporary relaxing of regulations with which healthcare practitioners formerly had to comply. HHS saw the massive need for accessible telehealth services, and rightly recognized that in this public health emergency, HIPAA compliance was an obstacle to the speedy expansion of telemedicine.

The agency acknowledged that “some of these technologies, and the

manner in which they are used by HIPAA-covered healthcare providers, may not

fully comply with the requirements of the HIPAA Rules.” Therefore, HHS chose to

“exercise its enforcement discretion” by refraining from “impos[ing] penalties

for noncompliance with the regulatory requirements under the HIPAA Rules…in

connection with the good faith provision of telehealth during the

COVID-19…emergency.”

Many telehealth platforms, remote monitoring tools, and health apps

are not really HIPAA-compliant. And nearly two years on, the “temporary” HIPAA

suspensions are starting to feel permanent.

Hackers

Target Health Data

There’s no question that sensitive

medical data gathered by health apps, telemedicine platforms, and EMR systems is

vulnerable to both marketing misuse and cyberattacks.

High-profile hacks targeting government agencies and private

companies alike regularly make news headlines. Healthcare organizations, from

hospitals to health plans to practitioners themselves can be targets of cybercrime

— a threat that’s escalated significantly in the past year.

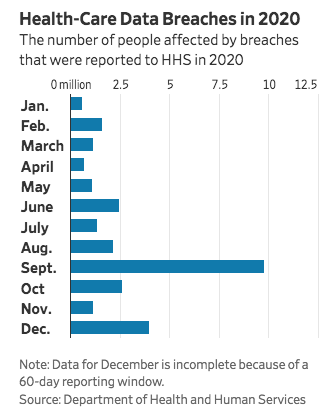

HHS indicates a 25% increase in healthcare data breaches in 2020

over 2019, itself a record-breaking year. In 2020, the department recorded thehighest total of large health data breaches –1.76

incidents per day on average–in any year since it began tracking the problem

in 2009. Officials have warned medical groups of a rise in hacking attempts

during COVID, in part stemming from cybercriminals’ efforts to steal

vaccine-related research and other medical data.

Aware of these threats, some politicians are advocating for tighter

federal data privacy and security laws. US Representative Suzan DelBene (D-WA)

introduced legislation last March that, if passed, would create the country’s

first-ever national data privacy standards.

TheInformation Transparency and Personal Data Control Act seeks to

protect individuals’ personal identifying information, including data relating

to financial, health, genetic, biometric, geolocation, sexual orientation,

citizenship and immigration status, Social Security Numbers, and religious

beliefs. It also protects all information pertaining to children under age 13.

Further, it would strengthen the Federal Trade Commission’s capacity to enforce

privacy rights and punish bad actors.

That’s good as far as it goes. But, notably, the bill does not

mention either AI or facial recognition technologies, or the ways in which they

capture consumer data.

Meanwhile, the use of these technologies—and in some cases, their

exploitation–is only accelerating within and beyond the healthcare realm.

AI-driven systems do indeed hold tremendous potential to transform

medical care for the better. But these advances do have downsides—both

predictable and unexpected. It is naïve to think otherwise.

Data

from a survey of over 3,500 functional, integrative, and metabolic medicine practitioners

suggests that most are navigating the stormy post-COVID waters with

considerable resilience.

Compared

with other physician surveys posted over the course of the last 9 months, the functional

and holistic clinicians in this cohort report fewer practice closures and less income

loss.

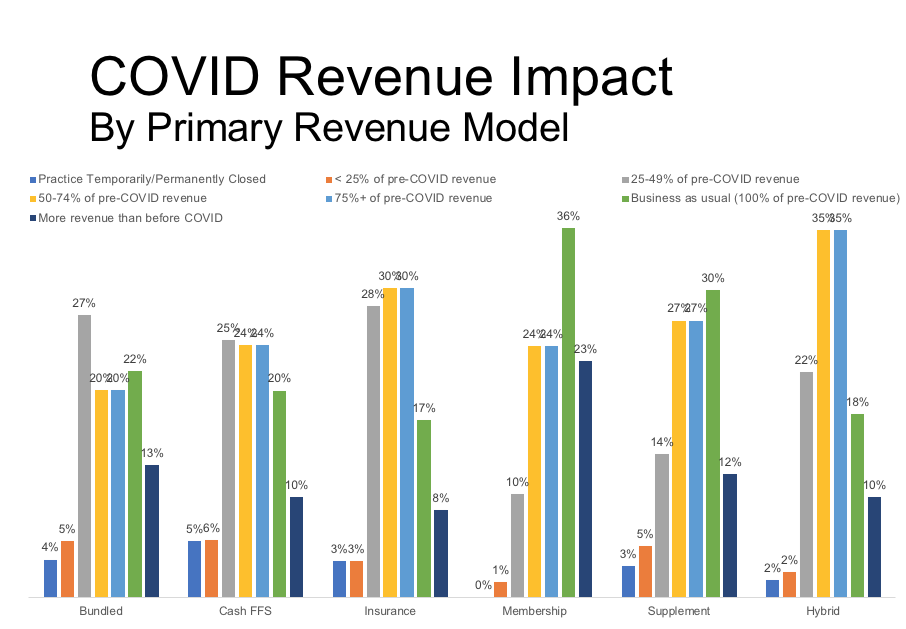

OvationLab’s COVID impact survey of more than 3500 functional/holistic medical practices indicates that overall, COVID-related practice closure rates are under 5%. Many practices have experienced significant revenue loss. Not surprisingly, membership/concierge practice models were best able to maintain pre-COVID income. (Data copyright OvationLabs)

Membership

(aka “concierge”) and bundled practice models appear to be protective against

the economic forces that have hobbled many conventional insurance-based

practices in the wake of COVID. This is especially true for small, independent practices.

This

new 33-question survey was fielded from late August through early September by OvationLab, a strategic consulting agency for the health, wellness, and

nutrition space. OvationLab’s principals—Laurie Hofmann, Andie Crosby, and Tom

Blue—have all served in leadership roles at the Institute for Functional Medicine for many years.

“This is a triumph for value-based medicine over conventional fee-for-service insurance models. There’s never been a better rationale for conventional practitioners—especially those in independent practices– to expand their capabilities, and to learn to apply root-cause medicine.”

—Tom Blue, OvationLab

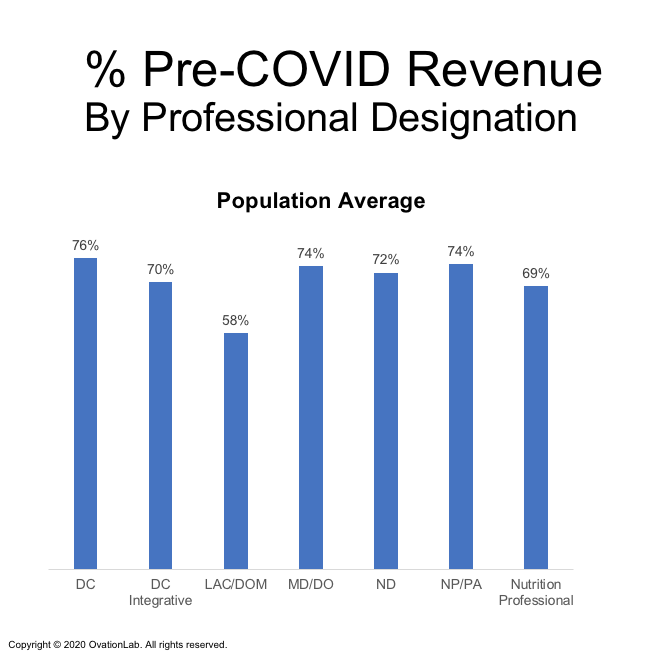

They

obtained 3,505 responses, representing clinics from all across the nation. MDs

and DOs make up 28% of the total, with naturopaths, nurses, and integrative chiropractors

representing 12% each. Eighteen percent are “straight” chiropractors, the

remainder represents a mix of nutrition professionals, acupuncturists, and others.

Roughly

two thirds are female, and the average age was 54.

The

respondents work in a wide range of practice models including conventional

insurance-based practices (29%), direct fee-for-service (46%), membership (aka

“concierge”) practices (5%), Bundled or fixed-price programs (4%), and hybrid

models (9%) that combine conventional insurance with low-level engagement in

direct pay, bundled programs, group visits, or other revenue models.

An

additional 7% have practices in which supplement sales are a major revenue source.

Few

Closures

COVID-related

practice closures were far lower among functional/holistic medical practitioners

compared with physicians as a whole. The closure prevalence in this cohort ranged

from 2-13%, depending on practitioner type. It was lowest among the MDs, DOs,

and NDs (2%), and highest among the acupuncturists (13%), the “straight”

chiropractors (5%), and nutrition professionals (5%).

There

were no closures among doctors who run membership or bundled service practices.

Among insurance-based practices, the closure prevalence was 3%; it was 5% in

the cash fee-for-service segment.

This

compares favorably against data from a Physicians Foundation (PF) survey

published in August showing that 14.5% of 3,513 respondents had closed their

practices, and an additional 4% expected to close over the course of the year.

Most of the closures (76%) were among independent private practices.

There were no closures among doctors who run membership or bundled service practices. Among insurance-based practices, the closure prevalence was 3%; it was 5% in the cash fee-for-service segment.

A

regional survey in April by New York University’s School of Global Public

health showed 15% of metro-NYC area practices were temporarily or permanently

closed due to lack of PPE, insufficient staff, or drastic declines in patient

volume and revenue.

Impact

on Income

Though

closure rates were low, OvationLab’s data show that many functional medicine

practices have borne revenue shortfalls. Upward of 75% of respondents were

economically impacted in some way. Between 20% and 25% are operating at 25-49%

of their pre-COVID revenue levels, and between 1% and 11% are getting by on

less than 25% of pre-pandemic income.

On

the positive side, roughly one-fifth of the respondents say that their income

has remained at pre-pandemic levels, and 7% to 14% say it has actually increased

over the last 9 months.

All of the practitioner subsets experienced significant declines in practice revenue due to COVID-19. Acupuncturists and practitioners of Oriental Medicine were hit the hardest

In

contrast, the PF estimates that 16% of the total US physician workforce—that’s

roughly 134,000 doctors—have changed their practice patterns in some way that

temporarily or permanently disrupted continuity of care. In that survey, 72% of

physicians had experienced income reductions and 55% expected income drops by

the year’s end.

The

hardest hits have been on solo and small-group independent practices.

OvationLab’s

Tom Blue points out that the vast majority of holistic and functional

physicians fall into that independent solo or small-group bracket, and it seems

they are faring considerably better than their peers in conventional practice.

Membership

Has Benefits

Though

only 5% of OvationLab’s cohort run membership practice models, these proved

extremely resilient to the post-COVID economic assault.

None

of the membership practices had closed, 36% reported they were operating at

“business as usual” revenue levels (100% of Pre-COVID), and 23% say revenue is

up.

Among

those clinics deriving a major portion of their income from bundled clinical

services—things like cardiovascular risk reduction programs, weight management

groups, and hormone replacement protocols—22% have maintained pre-pandemic

income, and 13% have seen revenue increases.

In

contrast, only 17% of the insurance-based practices maintained their pre-COVID revenue,

and just 8% saw increases.

Some

clinics offering bundled services did see revenue drop; 28% reported a 50% or

greater revenue hit due to COVID. In contrast, only 10% of the membership

practices saw such big revenue declines.

Practices that completely ignored COVID, and offered nothing specific to support patients concerned about the virus are worse off because of this. On average, these practices have generated 13% less revenue than those offering at least one COVID-related services.

Overall,

the findings do suggest that membership and, to a lesser extent, bundled

practice models provide independent practices with some protection against the

economic and social forces that drove many insurance-based indie practitioners

to shut their doors during the pandemic’s first wave.

“When

you look at the active patient census of membership practices collectively

across the country, you can’t even tell that COVID happened. According to data

from Hint Health, the largest membership payment processor for the concierge and DPC

industry, membership practices collectively grew 4% between March and July,”

Blue says. Hint processes patient payments for roughly 1,000 practices around

the US.

“They

ran the numbers, and nationwide, there was no net attrition (in patient

membership payments) over the 60 days in total shutdown. In fact, it grew 1%,”

Blue told Holistic Primary Care. “A pandemic is not a smart time to fire

your doctor.”

Challenges

Ahead

The

economic tenacity of the membership model may be more a reflection of the

affluence of its patient base than of its intrinsic strengths. People who can afford to pay a monthly

out-of-pocket fee to join a clinic—typically in addition to, not as a

substitute for what they pay for standard health insurance—are generally

well-off and much less likely to be forced to choose between healthcare and

food or shelter.

Whether

the situation remains so sanguine for private-pay remains to be seen.

Many

well-paid white-collar jobs have been dashed during the pandemic, and more

could be lost in the coming months. While COVID has caused many more people to focus

on their health—and to recognize the limits of conventional medicine–it has

also put many in precarious fiscal straits.

“If

this carries on long enough it could become a big challenge for people to pay

for private-pay healthcare services,” Blue said in an interview with Holistic

Primary Care.

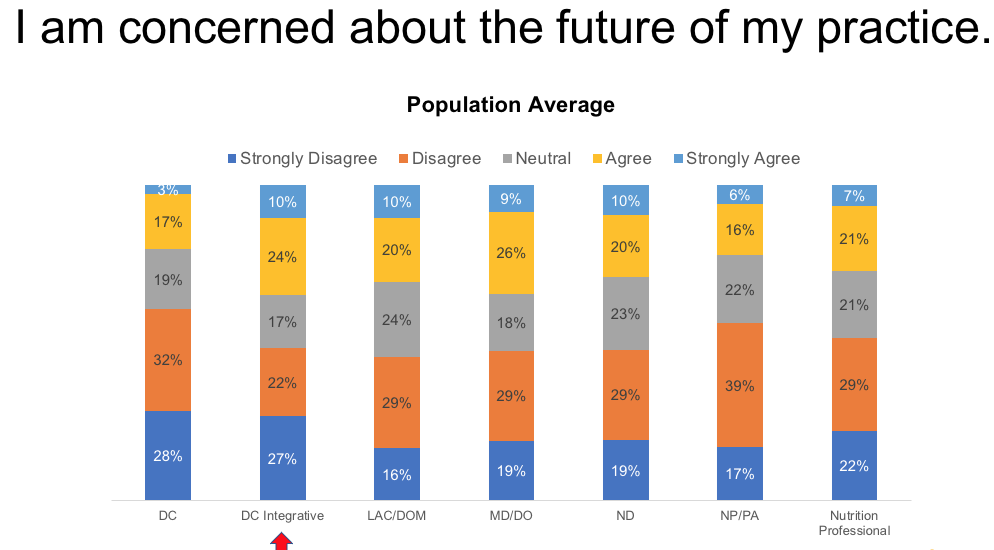

More than one-third of MDs, nearly one-third of integrative DCs, and 30% of naturopaths indicate that they are concerned about the future viability of their practices

“It

would be prudent to take a hard look at practice efficiency and optimizing for value,

which is basically outcomes over cost. We talk a lot about this, but in terms

of doing the work to optimize, that’s a big opportunity.”

“If this carries on long enough it could become a big challenge for people to pay for private-pay healthcare services.”

–Tom Blue, OvationLab

According

to an IFM survey, the throughput of a typical functional medicine practice is seven

patients per day, give or take. “If you bring this up to 12 per day– which is

still far less than in conventional care–it makes a huge difference

financially,” Blue says.

Group

Visits: No Panacea

The

business model that appears to be gaining the greatest traction is the use of

bundled programs. In OvationLab’s survey, 19% of the respondents indicate that

they are generating some revenue from this approach. But by and large, this

model is the exception, not the rule.

That

said, 54% of respondents agreed that they would implement bundled programs if

these were set up in a turn-key manner by trustworthy and experienced third

parties.

While

a growing number of practices are beginning to work with groups of patients,

either through group visits or group coaching and education programs, these

were not a meaningful source of practice income within the cohort.

“Some

of the most exciting implementations of group visits have taken place in health

systems like Cleveland Clinic Center for Functional Medicine. But the great

majority of our respondents are in independent practices,” Blue points out.

Telemed:

Finding the Right Mix

Telemedicine

is playing an important role in functional medicine practice survival during

COVID, but not exactly in the ways that one might assume.

Tom Blue, OvationLab

“The

practitioners that were doing 30% to 40% of their visits as virtual visits did

the best,” in terms of overall practice resilience, said Blue. “The doctors who

pivoted 100% to virtual visits fared worse and now have a significantly lower

percentage of their pre-COVID revenue.”

“The

healthiest practices have evolved to accommodate a continuum of patient

preferences with respect to virtual care. The big take-away seems to be to

focus on maximizing access and availability to patients in the ways that they

want to use the practice. That means offering virtual visits while maintaining

a brick-and-mortar presence.”

Contrary to what many might assume, the main determinant of practice viability during COVID was not the presence or absence of telehealth services, but the overall strength or fragility of the practice’s core revenue and patient engagement models.

One quarter of the MDs/DOs, one-third of the NDs, and nearly half

of the nutrition professionals in OvationLab’s cohort are doing more than 60% of

their total patient visits remotely.

Not surprisingly, engagement with telemedicine was much lower among

chiropractors and acupuncturists: Fully 85% of the straight chiropractors, 53%

of the integrative chiropractors, and 55% of the acupuncturists and doctors of

oriental medicine are not doing any virtual visits. The services they offer

simply cannot be done online.

While the respondents showed a generally high comfort level with

things like teleconsults, remote patient monitoring tools, and other big tech,

Blue says the processes of adaptation and technology implementation for the

COVID era are still very much underway for a lot of practitioners. Many

expressed the need for help in further integrating patient-friendly tech

solutions in their practices.

Contrary

to what many might assume, the main determinant of practice viability during

COVID was not the presence or absence of telehealth services, but the overall

strength or fragility of the practice’s core revenue and patient engagement models.

On that front, practices based on fee-for-service—whether direct pay or

insurance-based–appear to be the most vulnerable.

COVID

Care

Many

of the OvationLab respondents, particularly MDs, DOs, and nurse practitioners,

have treated patients with active COVID, though these cases represent a

relatively small segment of total patient consultations.

Just

over 60% of the MDs/DOs and roughly 55% of the NDs are offering some sort of

COVID-related services, such as COVID testing, antibody testing, monitoring or

ongoing support of infected patients, COVID prevention programs, or

“back-to-work” support programs contracted with employers.

Blue

says the practices that completely ignored COVID, and offered nothing specific

to support patients concerned about the virus are worse off because of this. On

average, these practices have generated 13% less revenue than those offering at

least one COVID-related services.

But

the COVID crisis creates a unique and

thorny paradox for practitioners: on the one hand there’s the imperative to educate patients and

provide the care they seek; on the other, patient-focused COVID communication

can easily cross the line into “marketing” or “false treatment claims” in the

eyes of the Federal Trade Commission and/or Food & Drug Administration. (Visit

www.HolisticPrimaryCare.net and watch our

webinar Your COVID Communications Could

Be Illegal)

Both

agencies have been aggressive in scrutinizing practitioners’ online messaging

about the pandemic. Since it began,

they’ve issued hundreds of warning letters to medical professionals requiring

them to delete COVID-related posts if they suggest specific treatments to

prevent or cure the syndrome.

Bottom

line is, it is easy to unwittingly step over the regulatory line. While it is

vital to meet patients’ needs for guidance, you need to be careful about how

you do that.

Better

COVID Outcomes?

There’s

some evidence from OvationLab’s survey that bundled services and membership

practices might deliver better overall outcomes for COVID patients.

Insurance-based

MDs and DOs who treated COVID patients reported hospitalizing 19% of their

infected patients, and had a 3.1% mortality rate.

The

MDs and DOs in membership practices reported a 7.2% hospitalization rate for

their COVID patients and only a 0.9% mortality rate.

The

analysis also showed that physicians who order a lot of advanced cardiovascular

lab work (Cleveland Heart Lab, Boston Heart Lab, PULS), tended to have lower

COVID hospitalization rates (7.7%), and fewer COVID-related patient deaths

(1.8%) than the MD/DO cohort as a whole.

These

findings are intriguing but difficult to interpret: Are the lower

hospitalization and death rates truly due to the functional medicine approach?

Or do they reflect the fact that these clinics tend to serve affluent patients with

better overall health status and fewer risk factors?

With

respect to these particular observations, OvationLab cautioned that the total

number of respondents with heavy COVID caseloads is small, and all the numbers

are self-reported.

Value

Triumphs

Few

healthcare professionals are experiencing smooth sailing these days, and

functional medicine practitioners are no exception.

But

to OvationLab, the message from their survey is very clear: the principles of

root cause medicine combined with value-based practice models have been

profoundly protective of independent practices during the COVID crisis, at

least so far.

“This

is a triumph for value-based medicine over conventional fee-for-service

insurance models. There’s never been a better rationale for conventional

practitioners—especially those in independent practices– to expand their

capabilities, and to learn to apply root-cause medicine,” Blue told Holistic

Primary Care.

According

to Patrick Hanaway, MD, head of the IFM’s COVID-19 task force, many physicians

are doing just that. “At our Annual International Conference (held online this

year), we had 50% new people. That’s just amazing to have that many people

engaging with the functional medicine conference for the first time. Usually, it’s

around 25-30%.”

The

surge is partly due to the fact that this year’s online conference was simply

more accessible, and did not carry the costs and time-burdens of travel.

But

Hanaway also sees it as an indicator that COVID has made more physicians aware

of the limits of drug-based care models.

“There’s

an openness to other tools. They’re looking to see what can I do to protect

myself, what can I do to help my patients? What can I tell patients about how

to enhance their immune systems, reduce symptoms, reduce transmission? All

those things are very important, and we’ve got tools.”

The COVID-19 pandemic has had profound impact on all aspects of healthcare. Holistic, functional, and naturopathic medicine are no exceptions. Some of these changes are positive, opening new opportunities for natural medicine to demonstrate its value. Others pose serious challenges.

Positive

or negative, the impact of COVID will be felt long after the virus is

contained.

Learn

how practitioners—and organizations that represent them—are adapting to the

“new normal,” how the regulatory and medicolegal landscape is changing, and what

the post-COVID future might look like.

This free half-day program features presentations from leaders of the Institute for Functional Medicine, and the Academy of Integrative Health & Medicine, as well as regulatory experts, patient survey data, and perspectives from Holistic Primary Care.

Virtual

practice has become a necessity in the COVID era, and telemedicine will likely

continue to expand even after the pandemic wanes.

For

practitioners of holistic and functional medicine, the dispensing of

supplements and other products is a vital component of both in-person and

virtual practice. But managing dispensaries whether online or in-clinic, can be

tedious and time-consuming.

Fullscript,

one of the world’s leaders in online dispensing and product distribution, is working

to simplify the process.

With

the launch in October of its new comprehensive platform, Fullscript is making

it possible for clinicians to manage their direct-to-patient online

dispensaries and their in-clinic product procurement “all from the same

account, in the same browser tab,” says Bruce Smith, Fullscript’s senior

manager of public relations.

Full Integration

The

new platform represents a complete integration of the original Fullscript

system with Natural Partners’ distribution and dispensing capabilities. The two

companies merged in 2018, but have maintained separate dispensing platforms and

distinct branding.

The

new platform is part of a broader effort to streamline, simplify, and optimize

the systems, so they best support practitioners and their patients.

“We have a lot of practitioners who like virtual dispensing. It is simple for patients, there’s no inventory to manage, nothing goes out of stock or out of date,” says Smith. At the same time, many clinicians continue to maintain in-clinic dispensaries, even in the wake of COVID.

The

new platform provides an easy way to administer both.

“There are lots of technologies and apps out there (to support virtual practice),” Smith told Holistic Primary Care. But managing them can be problematic. Our aim was to design something where you can do everything via one account.” The platform is built around the Fullscript – Natural Partners catalog of over 300 practitioner-facing supplement brands.

He

added that, “This is the most significant upgrade we’ve done on the Fullscript

side.” The company launched the new platform after several months of

beta-testing with hundreds of practitioners and their patients.

Comprehensive Practice Support

The

new platform is designed to be much more than simply an online dispensary; it

is a comprehensive practice support system that facilitates ongoing

communication between practitioners and patients, Smith explained. This can

increase patient adherence to treatment suggestions, potentially improving

clinical outcomes.

It

can be integrated with electronic health record systems, and offers a number of

“one-to-many” care tools. Practitioners can also use it to disseminate

automated wellness-oriented self-care content to patients.

System

users get access to the Fullscript

Knowledge Center , which compiles scientific content and commentary from leading holistic,

functional, and integrative medicine practitioners. There’s also a feature called Shareable Wellness Protocols,

that enables practitioners to share specific treatment protocols, product

instructions, and support messages to their entire patient database.

Fullscript

has a fully-dedicated in-house support team to help practitioners implement and

trouble-shoot the new system, which was developed with input from the company’s

medical advisory board: Tieraona Low Dog, MD; Jeffrey Bland, PhD; Joseph

Pizzorno, ND; Robin Berzin, MD; Cheng Ruan, MD; and Jeffrey Gladd, MD.

Founded in 2012, in Ottawa, Fullscript has was already experiencing rapid growth when the company merged with Natural Partners in 2018. The alliance brought together Fullscript’s technological strengths with NP’s distribution capacity and its long legacy as one of the mainstay distribution channels in the holistic and naturopathic world.

Alex Keller, ND, Medical Director, Fullscript

Since

the COVID pandemic hit the US, Fullscript Natural Partners has experienced 20%

to 30% growth in the number of new practitioners signing up each month, says

Alex Keller, ND, Fullscript’s medical director, in a webinar hosted by the

Council for Responsible Nutrition last July. The strongest growth has been

among medical doctors and chiropractors.

Poised for Rapid Growth

That

surge is strongly linked to the sudden embrace of telemedicine that has

happened in the wake of COVID. “Prior to COVID only about 5% of our

practitioners worked completely virtually,” Keller said reflecting on data from

a survey of 500 Fullscript practitioners. “Now, 60% are exclusively working

virtually.”

Fullscript

currently has 75,000 registered practitioner accounts, and now serves close to

1.75 million patient accounts.

For

the time being, the merged companies will maintain both the Fullscript and the

Natural Partners brand identities, though they will both operate via the

unified platform.

Eventually, though, the company will sunset the Natural Partners brand. “There’s no firm timeline yet on when that will be,” says Smith. “When the time does come we’ll give Natural Partners customers all the personalized support they need to use the improved experience on Fullscript.”

The COVID crisis has catapulted telemedicine and patient remote monitoring onto healthcare’s center stage

Patient self-assessment tools, along with remote consultation technologies, have evolved rapidly over the last decade. Until recently, they’ve been considered luxuries for highly motivated patients and future-forward clinicians.

In the post-COVID world, where many

physicians have closed their clinics and patients are deferring all but the

most essential in-person visits, telemedicine and remote monitoring are no

longer luxuries, they’re necessities. And they will shape the future of

clinical practice—especially in preventive medicine.

Here are a few home monitoring and self-assessment

strategies that allow patients to take more active roles in their care, while providing

practitioners with pertinent information to guide them along the way.

Befriend Technology

The current situation is obliging all of us in medicine to befriend new technologies. I have found a few basic tracking devices particularly helpful. These gadgets are user-friendly and built for ease-of-use at home. They can accurately track various health measurements and are compatible with many different wireless and internet platforms. They make it easy for patients and their practitioners to view and manage health data together as a team.

Omron blood pressure remote monitoring device

Blood Pressure Monitor: Maintaining a healthy blood pressure is essential. I suggest using a device like the Omron wrist blood pressure monitor. It is lightweight and portable, allowing patients to track their blood pressure on the go. It stores the readings, and the app interfaces with the patients’ computers, so they can keep and share comprehensive records of their recordings. I personally find the wrist version less cumbersome than the arm version.

Digital Stethoscope: Digital stethoscopes such as Eko stethoscopes use Bluetooth to pair with smartphones and tablets through the Eko App. Clinicians can listen to, visualize, and share auscultations of the same quality as if they were listening directly to their patients’ hearts in person, through ordinary stethoscope earpieces. This foregoes the need for close doctor-patient contact. Wireless stethoscope technology makes telemedicine exams much easier.

Assessing Cardiovascular Function

Heart Rate Monitors: The Resting Heart Rate is the number of times the heart beats per minute when someone is at rest. A good time to check this is in the morning after a good night’s sleep. For most of us, the RHR is between 60 and 100 BPM. But this can be affected by factors like stress, anxiety, hormones, medication, and level of physically activity. Athletes and highly active people may have RHRs as low as 40 BPM. When it comes to RHR, lower is definitely better, because it means that the heart muscle is in better condition and doesn’t have to work as hard to maintain a steady beat. Studies show that a higher RHR is linked with lower overall fitness, higher blood pressure, and overweight.

The Peak Heart Rate is 85 to 100 percent of someone’s maximum heart rate. I like to strive for a resting pulse rate of 50 BPM or less while asleep, and not more than 100 BPM when active.

Most of the current generation of smart phones come with the capacity to monitor both resting and peak heart rates. There are dozens of heart rate monitoring apps that make use of this built-in capacity to provide quick and easy analyses, no math required. I recommend looking for one that suits your patients’ needs. They are very useful.

AliveCor’s Kardia smartphone-based EKG monitoring system

Detecting Atrial Fibrillation (AFib): The irregular heartbeat patterns associated with AFib can lead to blood collecting in the heart, which can form stroke-causing clots. Tracking Afib at home is pure common sense. Just over two years ago, the FDA approved the AliveCor Heart Monitor— a smartphone app plus a special phone case with a set of sensors. Together they convert the phone into an EKG machine that patients can carry around in their pockets or purses. It allows you and your patient to see a simple version of the heart’s electrical activity in real time on the phone screen.

The system is very easy to use. A patient activates the app, places the index and middle fingers of each hand on the sensor pads, and records an EKG tracing. In the latest version, called Kardia, the sensors just need to be near–not necessarily on– the phone.

Heart Rate Variability & Autonomic Nervous System Assessment: The effect of heart activity on brain function—and vice versa–has been researched extensively over the past 40 years. Early research mainly examined the effects of heart activity occurring on a very short time scale – over several consecutive heartbeats at maximum. Scientists at the HeartMath Institute have extended this research by looking at larger-scale patterns of interaction between the heart, the brain, and the nervous system.

Heart rate variability (HRV) is a measure of the beat-to-beat

changes in heart rate. The normal variability in heart rate is due to the

synergistic action of the two branches of the autonomic nervous system (ANS).

The sympathetic nerves accelerate heart rate, while the parasympathetic (vagus)

nerves slow it down. The sympathetic and parasympathetic branches of the ANS

are continually interacting to maintain cardiovascular activity in its optimal

range and to permit appropriate reactions to changing external and internal

conditions.

HeartMath’s Emwave system measures heart rate variability, providing a valuable window on autonomic nervous system balance.

With that in mind, analysis of HRV over the course of someone’s day therefore serves as a dynamic window into the balance of the autonomic nervous system. While this seems complicated, it can be tracked fairly easily via a set of user-friendly smartphone-based tools. I recommend looking at Heart Math’s devices & apps that patients can use to monitor their HRV and self-entrain healthier, more coherent, and balanced physiological states.

Remote Lung Assessment

Spirometry & Lung Function Assessment: For patients with asthma, and others in need of frequent and regular spirometric testing, the Aluna Spirometer is the perfect solution. It enables patients to measure their lung function at home, which is a great asset for those who’ve had COVID or who are at high-risk, as it can potentially eliminate clinic visits.

The Aluna remote spirometry device was designed especially for kids with asthma, but it is also helpful for anyone–young or old–who needs frequent assessment of lung function.

The Aluna system consists of a special breath test device that links wirelessly to a smartphone, and an app for collecting the spirometry data. It calculates FEV1 instantly, and records, stores, and shares the readings. The app also has a medication utilization tracker, and a video game component—particularly well-suited to children and young patients—that explains what the readings mean and allows users to set lung function goals.

Aluna gives doctors an online dashboard on

which to monitor their patients’ spirometry data as it is being collected. Alternatively,

patients can choose to share the results over the internet. Aluna can help doctors

and patients work together to build a more precise, customized treatment plan

that keeps patients engaged in their own self-care.

In addition to these helpful devices and smartphone systems, there are 5 low-tech self-assessments that I recommend that we all use routinely. You can find complete protocols for these simple self-assessments at https://www.perqueintegrativehealth.com/lifestyle/self-tests/.

Low-Tech Options

First Morning Urine pH: The first morning urine pH is a good indicator of the body’s mineral reserve and its acid/alkaline state. The body routinely uses overnight rest time to excrete excess acids. One’s capacity to do so varies based on toxin load, individual ability to inactivate toxins, and to excrete them. Using a pH test strip, this is a simple, inexpensive at-home test. Maintaining a pH within 6.5- 7.5 is ideal, indicating that overall cellular pH is appropriately alkaline. Cells in all tissues of the body function best in an alkaline state.

Digestive Transit Time: The state of one’s digestive system affects all aspects of health. Measuring digestive transit time gives an idea of how long it takes for food to be digested and for waste to be eliminated. The ideal transit time is between 12-18 hours. Most people who eat the standard American diet have transit times of 36-96 hours, which is detrimental to overall health.

With the help of a few charcoal capsules, patients can easily and painlessly find out how well their digestive organs are doing their jobs. This can help guide decisions about the amount of fiber, probiotics, and other digestive support they need.

C Cleanse: This test uses buffered vitamin C (ascorbate)–the body’s universal antioxidant—to identify a person’s risk of oxidative stress and extent of antioxidant protection.

The process involves taking buffered ascorbate powder in increments of 15 minutes till there is a complete evacuation of the GI tract, or a flush/cleanse is achieved (watery stools). In people who are generally healthy and getting enough vitamin C, this “C cleanse” protocol will give a result of ≤4g. But it is not uncommon to see results of 50, 75 or even 100g, indicating that someone is very deficient in ascorbate. I recommend doing the C cleanse every week.

The skin-pinch test is a simple way for patients to assess their hydration level

Wrist Skin Pinch Test: Drinking enough water each day is crucial for many reasons: to regulate electrolyte balance, support kidney function, keep joints lubricated, prevent infections, deliver nutrients to cells, and keep organs functioning properly. Being well-hydrated also improves sleep quality, cognition, and mood.

A simple

self-test for hydration status that I like to recommend is called the wrist

skin test:

–

Gently pull up about ½ inch on the skin on the back of the wrist with the hand

extended out (not flexed either up or down).

– On releasing the pinch, if the skin immediately flattens, it is a sign of well-hydrated tissues. However, if the skin maintains a little ‘tent’ i.e., stays pinched and then slowly goes back to normal over 5-10 seconds, it is usually a sign of significant dehydration

Urine Specific Gravity (SG): Urine specific gravity is another important measure of hydration and kidney health that can be used to assess the kidney’s ability to concentrate or dilute urine. Ideally, urine SG measurements will fall between 1.002 and 1.030 if the kidneys are functioning normally. Numbers above 1.010 can indicate mild dehydration. The higher the number, the more dehydrated someone will likely be.

Measuring specific gravity of urine with a refractometer

I like to use a refractometer

for this test which projects light into the sample and helps determine the

density of the urine.

There’s no question that the COVID pandemic has moved telemedicine

and remote monitoring from the margins of healthcare into the mainstream. In

many ways, this shift provides new opportunities for patient empowerment and

practitioner emancipation.

Office visits will always have a prominent place in medical

practice, but they need not be the default setting for everything.

Telemedicine is not the be-all, end-all solution to the problem of healthcare access—many people do not own smartphones or computers—but this technology can help many people improve their health and wellbeing in ways that are convenient and affordable. It opens exciting new possibilities for how we practice and experience healthcare—possibilities we are just beginning to explore.